Kakebo method: the Japanese habit that changes how you manage your money

In a world dominated by digital and invisible transactions, losing track of our cash flow is easier than ever. The Kakebo method, a centuries-old Japanese tradition, emerges as the ultimate tool to close the gap between what we think we spend and the reality of our finances.

It is not just a saving technique, but a mindfulness exercise that transforms expense tracking into a strategic habit. In this article, we explore what it is, how it works, and the key steps to apply it and regain total control of your money.

What is the Kakebo method and where does it come from

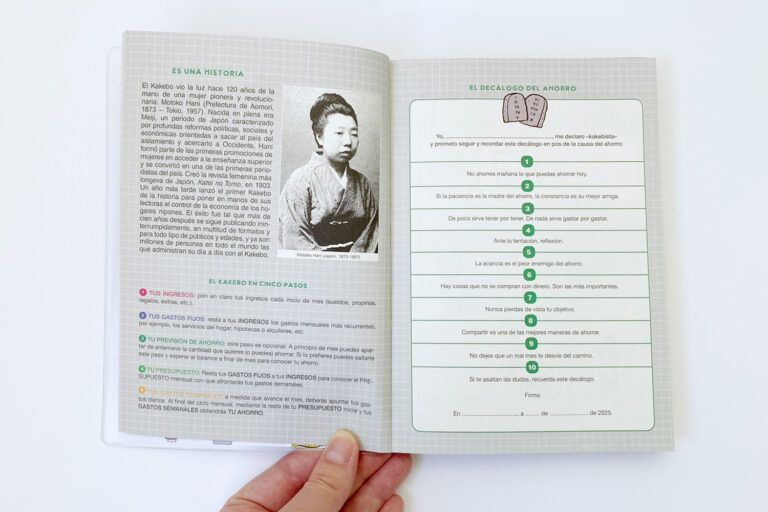

The Kakebo method literally translates as “household ledger for home economy.” Although today it is a global personal finance trend, its origin dates back to 1904 in Japan. It was designed by Motoko Hani, considered the first female journalist in her country and a visionary educator who founded the women’s magazine La compañera de la mujer.

Hani devised this system with a transformative purpose: to provide women with a tool for independence and self-sufficiency. At that time, they managed the family budget, and Kakebo allowed them to manage every yen with technical precision, turning saving into a path toward stability and personal empowerment.

Beyond being a simple accounting record, Kakebo is deeply rooted in the Japanese philosophy of minimalism and conscious reflection. Unlike today’s digital apps that automate the process, this method requires manual recording.

This action of “writing by hand” seeks to break the “autopilot” of modern consumption, forcing us to confront our habits head-on. Kakebo does not only ask how much we spend, but how those expenses reflect our priorities. By classifying money into categories (essentials, leisure, culture, and extras), the method teaches us to eliminate the superfluous to achieve a more orderly and satisfying life, aligning our finances with our personal values.

How the Kakebo method works

The success of Kakebo does not lie in forbidding you to spend, but in forcing you to look. By recording every coin that leaves your pocket, you break the “autopilot” of impulsive consumption. The method does not judge you; it simply gives you back a faithful reflection of your current priorities. The real reward is not just the balance in your account, but the peace of mind that comes from knowing, with absolute certainty, where every cent of your effort goes.

|

Stage |

When | Main action |

Objective |

| 1. Planning | Start of the month | Note income and subtract fixed expenses (rent, electricity, insurance). | Calculate the actual available budget. |

| 2. Commitment | Start of the month | Define a monthly savings amount and set it aside immediately. | “Pay yourself first.” |

| 3. Daily action | Every day | Record every variable expense, no matter how small. | Detect “small expenses” and leaks. |

| 4. Weekly control | Weekend | Add expenses by category and subtract from the monthly budget. | Assess whether you are on track or need to adjust. |

| 5. Final reflection | End of the month | Compare the savings achieved with the initial goal. | Identify which expenses were unnecessary. |

The four categories of Kakebo

For the analysis to be effective, Kakebo groups your outlays into four visual blocks (you can use colors to distinguish them):

- Survival (Essential):Food, transportation, health, housing. What you need to live.

- Leisure (Optional):Restaurants, pleasure purchases, tobacco, outings with friends.

- Culture:Books, cinema, theater, courses, or educational subscriptions. Kakebo gives special value to personal enrichment.

- Extras (Unforeseen):Home repairs, car breakdowns, unexpected gifts, or emergencies.

It is recommended to do this process by hand in a notebook. The physical act of writing reinforces the neural connection with your finances and makes you much more aware of the reality of your money than a simple digital app.

The four questions of Kakebo

At the start of each month, before writing down a single figure, and at its close, the method poses these four questions that act as a compass for your finances:

|

Question |

Strategic focus |

Purpose of the method |

| How much money do I have? | Awareness of starting point. Not just the bank balance, but the calculation of your net resources after subtracting fixed expenses (rent, utilities, debts). | Establish an honest and realistic starting point before the month begins. |

| How much do I want to save? | Active saving. Saving stops being “what’s left” at the end of the month and becomes a priority goal you set aside at the start. | Create a commitment with yourself and give purpose to your daily discipline. |

| How much am I spending? | Reality check. Answered through meticulous daily recording of every outflow of money, no matter how small. | Dismantle financial self-deception and bring visibility to expenses that often go unnoticed. |

| How can I improve? | Pattern analysis. It is the evaluation of the monthly balance where you identify which consumption habits you can adjust. | Plan a smarter and calmer next month, without recrimination and based on real data. |

Advantages and limitations of the Kakebo method

|

Aspect |

Real advantages |

Limitations and challenges |

| Complexity | Extreme simplicity. You don’t need financial knowledge or advanced software; just being able to add and subtract. Accessible for any age and type of economy. | Manual process. Not being automated, recording can be tedious or monotonous, especially after the first few months of use. |

| Control | Absolute awareness. By writing down every expense (even the cents), you eliminate self-deception and make visible the “leaks” that apps often ignore. | Receipt dependence. Requires collecting physical receipts or noting the expense instantly so as not to forget details, which generates resistance from people who prefer digital. |

| Habits | Progressive financial education. Encourages discipline, patience, and planning. Ideal for teaching the value of money to children and adolescents. | Demanding consistency. The biggest obstacle is perseverance. Many people abandon the method before completing the first quarter due to lack of habit. |

| Results | Achievable goals. Allows setting short-term objectives (like a trip or an emergency fund) in a very visual and motivating way. | Relative efficiency. For people who are already extremely frugal or organized, the method can add extra workload without providing new benefits. |

How to apply Kakebo today

Although Kakebo was born among paper notebooks and ink, its logic of “separate to control” is more relevant than ever in our digital age. Applying it today does not mean giving up technology, but using it so that the method is less tedious and much more tangible.

In the 21st century, manual recording can be supported by tools that automate discipline. While a spreadsheet or a Kakebo app helps with recording and charts, prepaid cards have become the perfect ally to materialize spending categories.

The strategy is simple: instead of keeping all your money in a single account where expenses get mixed together, you can use separate cards to protect your budgets. This is where tools like Bitsa come into play naturally. The method gives you the information; you decide the destination of every cent.